Addressing Two of the Most Tragic Misperceptions in Personal Finance

Become an Owner

When you begin to accumulate money, you may become overly concerned with protecting that nest egg.

“I’ve worked really hard for this money, I must maintain this balance and be conservative.”

But this short-term thinking negatively impacts your financial future.

There are many misperceptions in finance but arguably the two that are the most tragic include:

Underestimating your own longevity: How long you need to invest in assets that produce reliable income that protects your purchasing power.

Overestimating the damage that temporary declines on your investments have on your long-term wealth.

The real risk is not that you will lose money on your investments.

It’s that you will out live the money you have.

Let’s say you want to retire at age 50.

If you prioritize your greatest asset, don’t be surprised if you live well into your 80s and 90s (I hope that is the case for most of us, all morbid jokes aside…)

You need to figure out how to create a reliable income stream for the next 35-50 years that is able to keep pace, and even exceed, the inflation rate over that time period.

As we have discussed before, the best way to accumulate and build wealth is to purchase real assets.

I don’t mean to insult you, but do you understand and realize how powerful owning a stock can be?

Investing in stocks gives your direct ownership of successful companies.

When you invest in the S&P 500 index, you immediately gain ownership in the 500 most profitable, most soundly financed, and innovative companies in America.

Not to mention these companies are run by some of the most extraordinary people in the world.

Do your research on some of these people: Warren Buffett, Tim Cook, Jamie Dimon, Jensen Huang, Phebe Novakovic, Satya Nadella.

I could go on but I think you get the point.

These brilliant people work tirelessly to find opportunities, cut costs, and deliver shareholder value, for us.

To put it another way, they work for us.

Sure, not every company will be successful and some may even commit fraud or other crimes that result in us losing our capital.

That’s why I’m a huge proponent for owning hundreds, even thousands, of companies via an index fund.

Chances are I will make more money and endure less stress along the way.

How can stocks be a game-changer for you?

Based on history, over an average 20 year period, stocks would have made you six times as much money as 3-month Treasury bills. An average total gain of just under 600% versus just under 100% (before inflation, too)1

Since 1970, the S&P 500 index has increased by 45x, the earnings these companies generate increased 40x, and the dividends they pay out to shareholders has increased 22x.

All while inflation has increased 8x…

Are you following me now?

Given all that’s transpired over the past few years, and the volatility you are seeing in the markets, let’s not lose focus of what matters most:

Remember - over the short-run, investors’ emotions tend to drive the stock market. But over the long-run, it’s the earnings that these companies generate that matters.

Don’t allow the current chaos to cloud your judgement as you may not be able to distinguish between temporary loss and permanent loss.

Keep in mind the end game - generating enough income to sustain your lifestyle throughout your retirement.

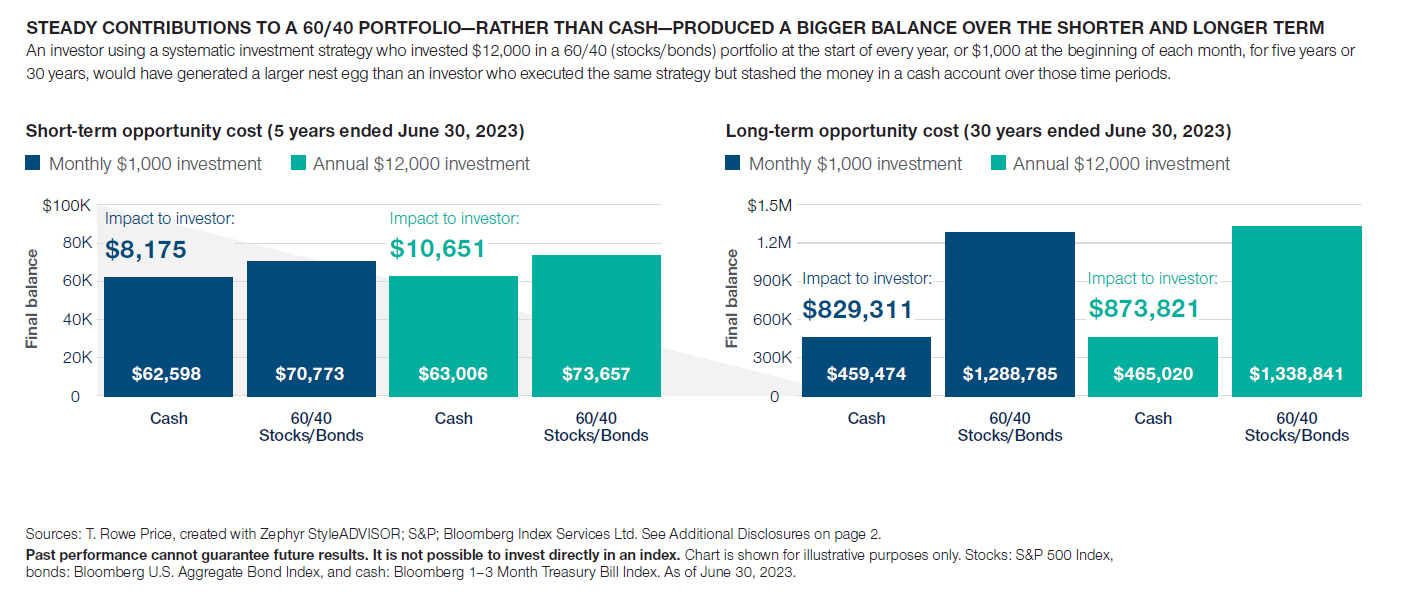

Even if you aren’t in 100% stocks, even a 60% stock, 40% bond portfolio, over the long-run, outperforms cash all. day. long.

Disclosure: This material is for general information only and is not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

All indices are unmanaged and may not be invested into directly.

All investing includes risks, including fluctuating prices and loss of principal.

Barron’s: https://www.barrons.com/articles/retirement-planning-mistakes-51671121778?mod=hp_DAY_Theme_1_3